Insurance coverage for prescription weight loss medications is defined by your plan type, your BMI, and the specific drug your doctor prescribes. This weight loss medication insurance coverage guide breaks down exactly how employer plans, Medicare, Medicaid, and marketplace policies handle GLP-1 and GIP medications like semaglutide and tirzepatide. As of 2026, about 43% of employer-sponsored plans cover GLP-1 medications for weight loss, rising to over 60% in large-group plans. That gap between large and small employers is one of the most consequential facts in the entire coverage landscape. Knowing which side of that line you fall on changes everything about your strategy.

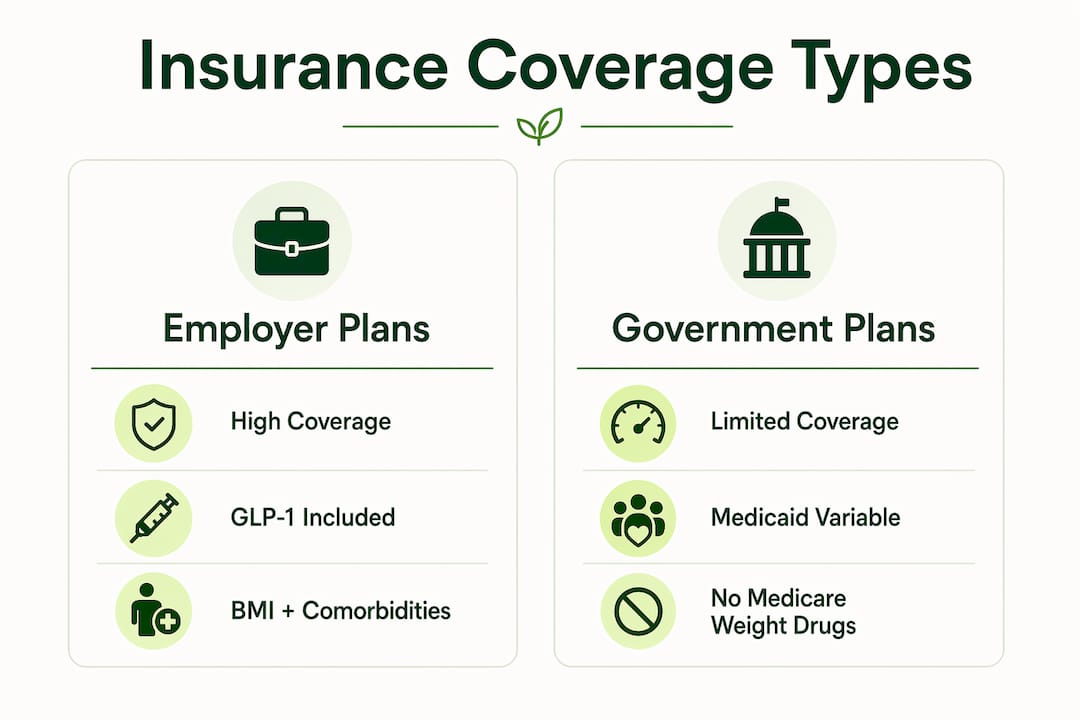

Coverage for obesity treatment depends almost entirely on which type of health plan you have. The rules differ sharply across employer, Medicare, Medicaid, and individual marketplace plans.

Large employers are the most likely to cover weight loss drugs. Over 60% of large-group plans now include GLP-1 medications on their formulary. Small-group and individual employer plans lag significantly behind. Even when a drug appears on a formulary, that listing does not guarantee coverage. Utilization management requirements like age thresholds, BMI minimums, and documented failed therapy history often determine whether a claim actually gets approved. Always check your Summary of Benefits and Coverage document, not just the drug list.

Medicare Part D is statutorily prohibited from covering drugs prescribed solely for weight loss. The one major exception: Medicare covers Wegovy when prescribed for cardiovascular risk reduction, with a copay cap of $50 per month. This means patients with a documented history of cardiovascular disease may qualify where others do not. If your doctor can tie the prescription to a cardiovascular indication, Medicare coverage becomes a real option.

Medicaid coverage for weight management medications is fragmented across states. Roughly 18 states include GLP-1 medications within their Medicaid programs, typically requiring a BMI of 30 or higher plus at least one qualifying comorbidity. States that do not cover these drugs often cite budget constraints. If you are on Medicaid, contact your state’s Medicaid office directly to confirm current formulary status, since policies change frequently.

Marketplace plans purchased through HealthCare.gov frequently exclude weight loss medications or place them on high-cost tiers. Individual plans outside the employer market follow similar patterns. Patients on these plans often face the highest out-of-pocket costs for GLP-1 medications.

| Plan Type | Coverage Likelihood | Key Conditions |

|---|---|---|

| Large-group employer | High (60%+) | BMI threshold, prior authorization |

| Small-group employer | Moderate | Varies by plan; often excluded |

| Medicare Part D | Limited | Cardiovascular indication required |

| Medicaid | Variable | ~18 states; BMI + comorbidities |

| Marketplace/individual | Low | Often excluded or high-tier |

Most insurers apply a standard set of clinical thresholds before approving medication coverage for weight loss. Meeting these criteria precisely is what separates approvals from denials.

The most common requirements are:

Formulary inclusion does not guarantee coverage. Insurers use utilization management rules to filter out patients who do not meet every condition. A drug appearing on your plan’s list means nothing if your documentation is incomplete.

Comorbidities carry more weight than BMI alone. Insurers are increasingly viewing obesity as a gateway disease with downstream costs tied to cardiovascular disease, diabetes, and joint deterioration. Framing your case around those conditions, not just your weight, is the most effective approach.

Pro Tip: Ask your doctor to document every weight-related health condition in your chart before submitting a prior authorization request. A diagnosis of hypertension or pre-diabetes listed in your medical record strengthens your case far more than BMI alone.

Getting insurance approval for a prescription weight loss medication follows a predictable process. Each step builds on the last, and skipping any one of them is the fastest way to get denied.

Verify your plan’s formulary. Log into your insurer’s member portal and search for the specific medication by name. Confirm it is listed and note which tier it falls on. Tier placement determines your copay.

Schedule a consultation with your doctor. Your physician needs to assess your BMI, document your comorbidities, and confirm that you meet the clinical criteria your insurer requires. Telehealth platforms like Oaklovesyou make this step accessible without an in-person clinic visit.

Compile your documentation. Gather records of prior weight management attempts. This includes food logs, gym memberships, records of previous medications, and any referrals to dietitians. Documented failed attempts over 3–6 months are one of the most common requirements insurers check first.

Have your provider submit a prior authorization request. The request must include a medical necessity letter, your clinical history, and documentation of prior treatment attempts. Incomplete submissions are the most common reason for initial denials.

Track the insurer’s response timeline. Most insurers must respond to prior authorization requests within 72 hours for urgent cases and 15 days for standard requests under federal rules. Follow up if you do not hear back within that window.

Know your appeal rights before you need them. If the request is denied, you have the right to appeal. Request the denial in writing and note the specific reason given. That reason determines your appeal strategy.

Pro Tip: Call your insurer’s pharmacy benefits line before your doctor submits the prior authorization. Ask specifically which diagnosis codes and documentation they require. Getting that list in advance prevents the most common submission errors.

A denial is not a final answer. The appeals process is a structured, multi-step pathway that ends with an independent external review if internal appeals fail.

The most common denial reasons are:

When you appeal, shift the focus of your medical necessity letter. Appeals succeed more often when the letter emphasizes comorbidities like hypertension and sleep apnea rather than BMI alone. Your doctor should frame the medication as treatment for those conditions, not just a weight loss tool.

“An effective appeal letter does not argue that the patient needs to lose weight. It argues that untreated obesity is worsening a serious medical condition that the insurer is already paying to manage. That reframe changes the insurer’s calculus entirely.”

If your internal appeal fails, the Affordable Care Act mandates access to an external review by an independent medical reviewer. External review under the ACA gives you a genuine second opinion outside the insurer’s own system. Patients who reach this stage and have strong documentation win a meaningful share of these reviews.

One more thing to know: compounded GLP-1 medications are almost never covered by insurance, even when the brand-name version is. If you are using a compounded version, expect to pay the full cost out of pocket. That is a critical distinction when planning your budget during an appeal period.

Getting weight loss medication covered requires the right plan type, complete documentation, and a willingness to appeal denials using comorbidity-focused medical necessity letters.

| Point | Details |

|---|---|

| Plan type determines coverage | Large-group employer plans cover GLP-1 drugs at the highest rates; individual and marketplace plans rarely do. |

| Documentation drives approvals | Insurers require BMI thresholds, comorbidity records, and 3–6 months of documented prior weight management attempts. |

| Medicare has one exception | Medicare Part D covers Wegovy only for cardiovascular risk, with a $50/month copay cap. |

| Denials are reversible | Appeals focused on comorbidities rather than BMI alone succeed at higher rates, especially with ACA external review. |

| Compounded drugs are not covered | Compounded GLP-1 versions are excluded from insurance coverage and typically cost $300–$500 per month out of pocket. |

The single biggest mistake I see is treating the prior authorization as a formality. Patients assume their doctor will handle it and that the insurer will approve it. Neither assumption holds up. The prior authorization is a clinical argument, and it needs to be built like one.

The coverage landscape in 2026 is genuinely improving. Insurers are starting to recognize that paying for obesity treatment now costs less than managing cardiovascular disease, diabetes, and joint replacement later. That shift in thinking is real, but it has not translated into automatic approvals. The documentation burden on patients remains high.

My honest advice: do not accept a denial without appealing. The external review process exists precisely because internal denials are not always medically sound. Patients who document their comorbidities thoroughly, work with a physician who understands the prior authorization process, and escalate through every available step win far more often than those who stop at the first “no.”

— Eric

Navigating insurance for weight loss drugs is complicated, but getting access to a licensed physician does not have to be.

Oaklovesyou is an online telehealth platform that connects you with licensed physicians who can assess your eligibility, document your medical history, and prescribe GLP-1 and GIP medications like semaglutide and tirzepatide. The process starts with an online health questionnaire reviewed by a physician, and approved prescriptions are delivered directly to your door. Oaklovesyou also provides 24/7 support and physician-led guidance throughout your treatment. If you are ready to take the first step, visit Oaklovesyou to learn more about your options.

Coverage depends on your plan type. About 43% of employer-sponsored plans cover GLP-1 medications for weight loss, with large-group plans exceeding 60% coverage rates.

Most insurers require a BMI of 30 or higher, or a BMI of 27 or higher with at least one documented comorbidity such as hypertension or type 2 diabetes.

Medicare Part D does not cover drugs prescribed solely for weight loss. The exception is Wegovy, which Medicare covers when prescribed for cardiovascular risk reduction, with a $50 monthly copay cap.

Request the denial in writing, identify the specific reason, and file an internal appeal with a medical necessity letter that emphasizes your comorbidities. If the internal appeal fails, request an independent external review under the ACA.

Compounded GLP-1 medications are almost never covered by insurance, even when the brand-name equivalent is covered. Patients typically pay the full out-of-pocket cost, which often runs $300–$500 per month.

.svg)

Get wellness tips, offers, and updates

in your inbox.

Call the clinic: 435-244-7757

By providing your phone number & email, you expressly consent to receive SMS, email, or Meta messages from Oak Longevity Holdings Corp., Flow Longevity Holdings Corp., Mito Health Holdings Corp., including both transactional communications (such as appointment reminders, prescription updates, order and shipping notifications, and customer support) and marketing communications (including promotions, discounts, product offerings, and program updates) across their affiliated brands and services. Message and data rates may apply. Consent is not a condition of purchase.

© 2026 Oak Longevity - All rights reserved.